How New Blockchain Apps Make It Easier To Use DeFi

June 25, 2021

The Dai Savings Rate (DSR) is one of the most anticipated features of Multi-Collateral Dai (MCD). First, the DSR will further differentiate Dai from other stablecoins. In addition to continuing to provide Dai holders with a stable decentralized currency, MCD will offer an option to earn savings simply by holding Dai. Any Dai holder may lock her Dai in a smart contract to earn additional Dai. Second, depositing and withdrawing Dai will happen via an easy-to-use dapp provided by the Maker Foundation. And finally, DSR will play a role in maintaining Dai’s soft-peg to the US Dollar by stimulating demand for Dai.

Lock-Up Dai to Earn Savings

At the launch of MCD, any Dai holder will be able to deposit Dai into the Dai Savings Rate smart contract to earn additional Dai. Think of DSR as a savings account for your crypto. The process is simple, as noted directly below and illustrated in Figure 1:

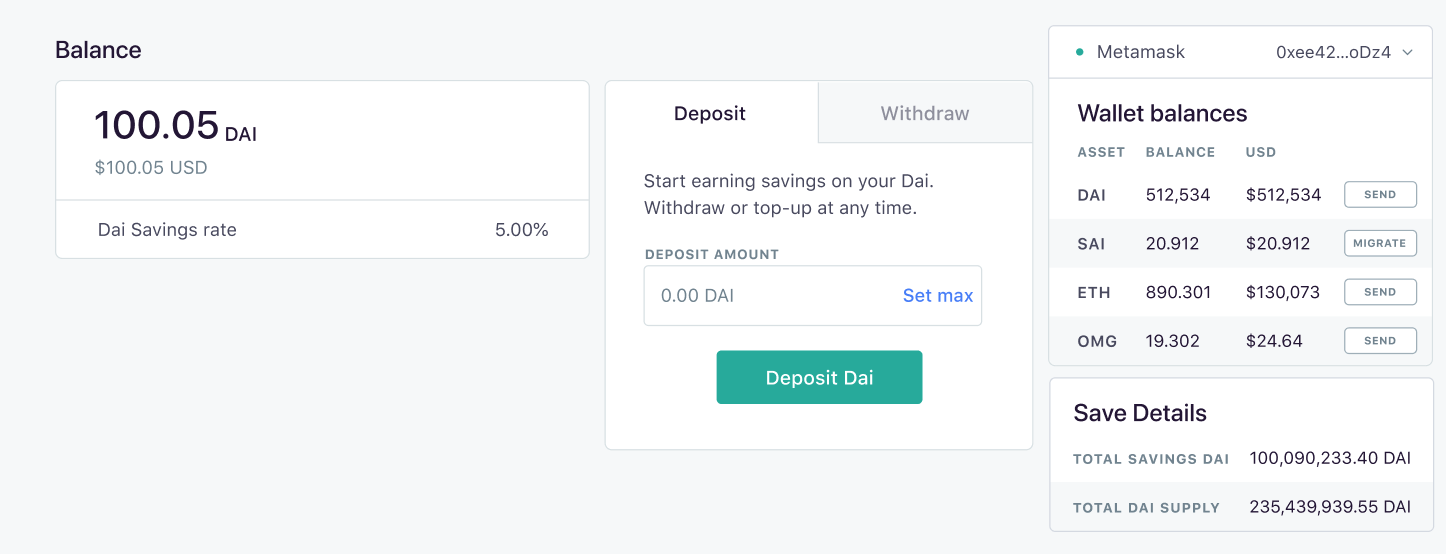

Dai holders will use a DSR dapp to easily deposit and withdraw Dai, and review other information. In the mockup below of the dapp for DSR, the user can see the total amount of Dai in their wallet (512,534 Dai) and the amount of Dai they have within DSR (100.05 Dai).

The user can easily top up their Dai in the dapp by specifying an amount in the “Deposit” tab, pressing the “Deposit Dai” button, and then signing the transaction. Likewise, Dai can be withdrawn from the DSR dapp and transferred back to the user’s wallet by specifying an amount in the “Withdraw” tab, pressing the “Withdraw Dai” button, and signing the transaction.

The success of DSR depends on attractive market rates that are sustainable for the Maker Protocol. So, let us now look at the Governance and Risk aspects of the Dai Savings Rate.

Governance and Risk

The Dai Savings Rate is expected to play a central role in MakerDAO governance, primarily as a tool to help maintain Dai’s peg to the US Dollar. In Single-Collateral Dai thus far, the lever used to maintain the Dai peg has been the Stability Fee. Changes to the Stability Fee, which are determined by Maker governance, incentivize CDP owners to borrow or repay Dai, consequently pushing the Dai price up or down until it equilibrates. By targeting Dai generation, this parameter impacts the supply side of Dai.

The DSR, however, offers an alternative tool for Maker governance. Because the DSR will influence Dai holders’ behavior (as opposed to the behavior of CDP owners), Maker governance can affect the demand side of Dai. End users will be incentivized to buy or sell Dai in the open marketplace based on how much additional Dai they may earn through the DSR. If the Dai price is too weak, the DSR may be raised, motivating users to acquire more Dai, and thereby pushing the Dai price up, closer to the peg. If the Dai price is too strong, it is expected that the DSR will be lowered to alleviate excess Dai demand, moving Dai prices down closer to the peg. Maker governance should be cognizant of these dynamics as they adjust the Dai Savings Rate.

Who Pays for the Dai Savings Rate?

Functionally, a design goal of the Dai Savings Rate is to ensure that excess Dai is not printed “out of thin air” (i.e., make certain that Dai minted for the DSR remains adequately backed by collateral). The implication here is that the DSR is a cost burden on some ecosystem actor. So, Maker governance should take into consideration who ultimately carries that burden and absorbs the cost.

At the accounting level, Dai awarded through the DSR is recorded in the same line item as the one used to record Stability Fees collected. In other words, the Dai created for the DSR is recorded as an offsetting adjustment of Stability Fees collected for the Surplus Auction. If the total amount of Stability Fees collected in Dai does not cover the total amount of Dai minted for the DSR, the difference is recorded as bad debt, and MKR is printed to cover the cost.

While MKR holders bear the ultimate cost of the DSR, the expectation has always been that CDP owners would effectively pay for it through a commensurate increase in the Stability Fee. Conceptually, the Stability Fee should be comprised of two components: 1) a collateral-specific risk premium that is a value transfer from CDP owners to MKR holders, and 2) a DSR adjustment that is a value transfer from CDP owners to Dai holders. Essentially, CDP owners compensate the two distinct ecosystem actors: MKR holders for the risk of collateral, and Dai holders for the risk of Dai instability.

There are additional complexities to consider with respect to collateral types. Specifically, global increases in Stability Fees due to the DSR may render certain collateral types as infeasible for inclusion. For example, if the DSR were set at 5% (thus causing a base Stability Fee of 5% on all collateral types), it would no longer make financial sense to include certain collateral assets that require a low cost of capital. A mortgage, for example, might have difficulty remaining competitive at >5%.

Taking these determinations to their natural conclusion, Maker governance will need to consider the following questions:

These are difficult questions, even in the presence of a long history of data analytics. As a result, the Interim Risk Team will propose to Maker governance that the full amount of the DSR adjustment not be passed globally onto all collateral types until a robust solution is devised and put into place. Instead, the portion of the DSR passed on to the Stability Fee should allow for inclusion of all collateral partners into the Dai Credit System. The shortfall will end up being a cost borne by MKR holders at the benefit of a flourishing collateral ecosystem.

To illustrate, consider a collateral pool of three assets with a cost of capital of 3%, 5%, and 10%. If the DSR adjustment required by the market is 5%, and that cost were to be passed on to the Stability Fee, then the first collateral would be priced out of the protocol. Therefore, Maker governance should consider passing only a 3% cost into the Stability Fee, and absorbing the other 2%.

Comparison to Other DeFi Platforms

As the Dai Savings Rate presents another savings vehicle for Dai holders in the broader DeFi ecosystem, it is important to understand its risk profile relative to other DeFi platforms. The key insight for understanding DSR is that it presents exactly the same risk as holding regular Dai. Unlike centralized savings products whereby a counterparty lends deposits in order to generate interest, DSR doesn’t have counterparty risks, as the Dai generated by it is programmatically minted, and it is guaranteed by the same backstops as regular Dai, namely MKR dilution. This makes DSR definitionally the least risky savings vehicle for Dai. Other savings vehicles in the DeFi ecosystem offering higher rates do so only at the cost of higher risk.

DSR Starting Values

Prior to the launch of MCD, the Maker community will have an opportunity to select (through a governance poll) a starting value for the Dai Savings Rate. Options will be chosen by the Interim Governance Facilitator and derived from a signal-gathering discussion in the MakerDAO Forum. While we expect plenty of debate on what the rate should be or which benchmark (if any) it should track, we suggest a simpler trial-and-error approach. After the initial parameter has been selected via a governance poll, the community should prepare for a rapid, iterative process until the DSR reaches its natural equilibrium, as evidenced by a stable Dai price.

Eventually, the DSR can be determined based on empirical data. As the models become more mature, Maker governance can start to manage the balancing effect necessary to attribute global or collateral-specific DSR values.

Summing It All Up

Here’s what we’ve covered above:

If you hold Dai, you will be able to lock-up your tokens and earn savings. If you hold MKR, prepare to participate in setting the Dai Savings Rate for the launch of MCD.

In the meantime, if you have questions or are curious as to what others in the community think, read our MCD-related blog posts and join the dialogue in the MakerDAO Forum.